Around the world, countries are searching for practical ways to cut emissions in sectors that cannot easily electrify. Few sectors are harder to decarbonize than shipping, which moves more than 80% of global trade and whose fuel choices carry consequences far beyond national borders. As LNG‑powered vessels continue to expand across major shipping routes from Asia to the Middle East, Europe, and the Americas the question is no longer whether LNG will play a role in the transition, but how quickly it can shift from fossil LNG to renewable LNG.

This is where liquefaction by equivalence enters the picture. Although the concept emerged in Europe, the challenge it addresses is global: how to turn renewable methane into renewable LNG at a scale and speed that matches the needs of international shipping.

To understand why this matters, and why the world is paying attention, it helps to look at the two cases presented in the webinar organized by the e-NG Coalition in March: Shell’s global market analyses and Engie Elengy’s operational experience in France. Together, they show both the scale of the challenge and the practicality of the solution.

LNG has become the most widely adopted alternative fuel in the maritime sector. Shell’s data shows that LNG‑powered vessels now make up the largest alternative fuel fleet worldwide, with hundreds more on order across container ships, car carriers, tankers, cruise vessels, and bulkers. This trend is not limited to Europe. Asian shipyards are building LNG vessels at record pace, Middle Eastern ports are expanding LNG bunkering capacity, and North American operators are increasingly turning to LNG for compliance and cost reasons.

The environmental benefits of LNG compared to conventional marine fuels are well documented. But the real decarbonization potential comes from replacing fossil LNG with bio‑LNG and e‑LNG (renewable methane). These renewable variants can reduce lifecycle emissions dramatically if they can be produced and delivered at scale.

And that is the bottleneck. Renewable methane production is growing, but not necessarily near the ports where ships bunker. Meanwhile, LNG terminals, where liquefaction capacity exists, are often located far from biomethane or e‑methane production sites. This mismatch between where renewable gas is produced and where renewable LNG is needed has become a global problem, because this geographic disconnect exists on every continent.

Liquefaction by equivalence is the bridge that can connect the two.

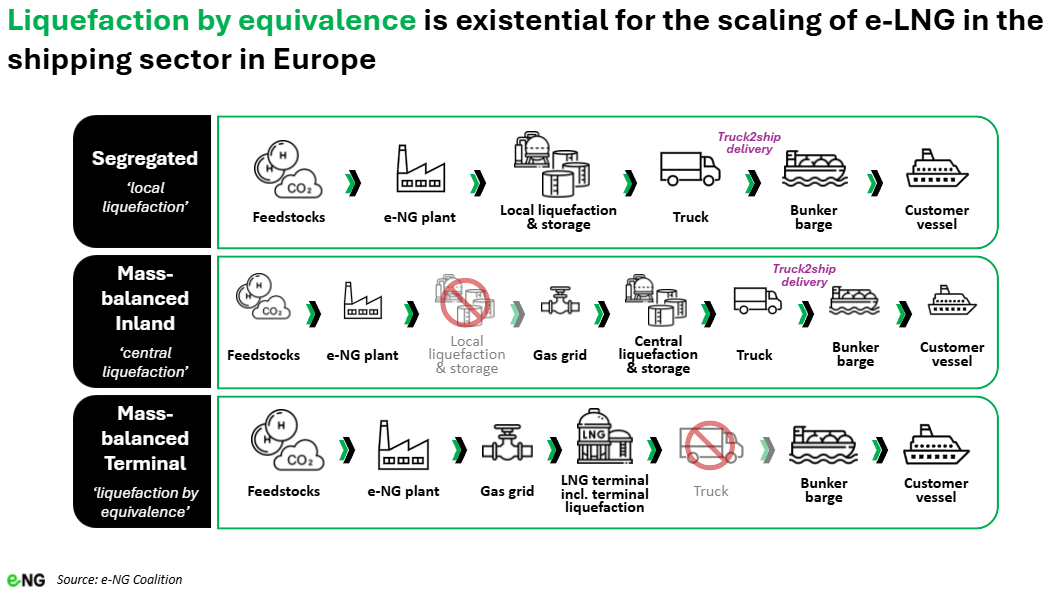

Liquefaction by equivalence allows renewable methane injected into a gas network to “be recognized as” renewable LNG at an LNG terminal, even when the physical molecule delivered at the terminal is not the same one injected upstream. It relies on mass balance accounting for a principle already well established worldwide for renewable electricity, sustainable biofuels, and green hydrogen certification.

The logic is straightforward: when a producer injects renewable methane into an interconnected gas system, and an LNG terminal subsequently liquefies an equivalent volume of gas, the renewable attributes can be transferred through certification. The physical molecules do not need to travel together; only the sustainability characteristics do.

This approach removes the need to build new pipelines, additional liquefaction plants, or dedicated storage facilities. Instead, it leverages the infrastructure that already exists with gas grids, LNG terminals, and bunkering networks to deliver renewable LNG where it is most needed, in the most efficient and environmentally sound manner.

France offers one of the clearest real-world demonstrations of liquefaction by equivalence. Engie Elengy, which operates three LNG terminals, has been applying this model under ISCC certification since 2024. Their experience shows how the system works step by step.

A biomethane producer injects renewable gas into the interconnected gas grid. A Proof of Sustainability (PoS) is issued for the injected volumes, specifying the terminal where the gas will be liquefied. When a customer arrives at the terminal to load LNG—whether into a truck or a bunker vessel—Engie Elengy verifies the PoS, checks that the customer has sufficient LNG in the tank to physically load, and then converts the biomethane PoS into a bio‑LNG PoS.

This conversion includes the carbon intensity of liquefaction and transport, calculated according to ISCC rules. It also ensures that customers cannot claim more renewable LNG than the biomethane they have injected or the LNG they have physically loaded.

The result is a certified renewable LNG product that can be used in fueling stations or maritime bunkering. Because LNG terminals operate at large scale, the model is suited to deep-sea shipping. As Engie Elengy notes, a single bunker vessel can replace hundreds of truck deliveries, making terminal-based liquefaction the only practical option for global maritime operations.

Importantly, this pathway reduces emissions at the system level. By using existing infrastructure efficiently, it avoids unnecessary liquefaction and regasification cycles, lowering overall energy use. Modern large-scale liquefiers would have even lower carbon intensity than the conservative values currently used in certification.

Shell’s contribution places liquefaction by equivalence in a global context. Their analysis shows that LNG demand in shipping is rising across all major regions and that LNG engines are already delivering environmental benefits. But the real challenge is scale. The renewable LNG volumes needed to decarbonize the global LNG fleet cannot be produced and liquefied locally everywhere.

Shipping is inherently international. Vessels bunker at major hubs such as Singapore, Rotterdam, Fujairah, Houston, and Shanghai, not in the rural areas where biomethane is often produced. Without a mechanism like liquefaction by equivalence, renewable LNG would remain limited by geography rather than demand.

Shell’s data makes the point: the only way to supply renewable LNG at the scale required by global shipping is to use the LNG terminals that already exist. Liquefaction by equivalence is the only pathway that aligns with this reality.

Although the regulatory debate began in Europe, the underlying issue is universal. Countries with large gas grids including the United States, Canada, Brazil, Japan, South Korea and Australia face the same question: how to connect renewable methane production with LNG demand efficiently, credibly and at scale.

As more regions develop biomethane and e-methane industries, the need for a harmonized, internationally recognized approach to liquefaction will only grow. Certification systems such as ISCC already operate globally, and mass balance principles are widely accepted in international energy markets. Liquefaction by equivalence fits naturally into this landscape.

Liquefaction by equivalence is already operational in several countries, supported by established certification systems, and increasingly embedded in the strategic planning of global energy companies building renewable LNG supply chains. Across the maritime sector, it is widely regarded as the only realistic pathway capable of decarbonizing the existing LNG-powered fleet at the scale and speed the industry requires.

It builds on the infrastructure the world already has, turning it into a platform for the renewable fuels the world urgently needs. The approach is technically robust, economically efficient, and fully aligned with the principles of technology neutrality and mass balance accounting that guide modern energy markets.

As countries update their regulatory frameworks, the moment is here: to choose a pathway that is environmentally credible, operationally workable, and capable of scaling globally. Liquefaction by equivalence delivers exactly that.

Beyond its global relevance, the recognition of liquefaction by equivalence in the EU regulatory framework, through RED III, the Implementing Regulation 2022/996 and the Union Database (UDB), is not a marginal technical adjustment. It is an existential precondition for the entire bio-LNG and e-LNG value chain.

A regulatory recognition without operational anchoring is meaningless. The current text of Implementing Regulation 2022/996 already allows liquefaction by equivalence within interconnected gas infrastructure. However, without a clear methodology in Annex VI of RED III, without operational rules in the revised Implementing Regulation, and without proper integration in the UDB, this pathway cannot be used in practice for compliance purposes neither under FuelEU Maritime, nor under the EU ETS, nor under the RED transport sub-targets. The legal basis exists; what is missing is its operationalization across the three instruments.

Avoiding double counting is the core of the issue. Mass balance accounting only works if emissions are attributed to the right value chain. Upstream LNG production and transport emissions belong to the fossil value chain, where they are already accounted for and assigned to fossil consumers. Re-attributing these same emissions to the green molecule injected and certified separately would create a double allocation: the same physical emissions would be counted twice once in the fossil ledger, once in the green one. This is not a fair reflection of reality; it is a methodological error that would undermine the integrity of GHG accounting and contradict the very principles that govern certified renewable electricity, sustainable biofuels and green hydrogen.

Without equivalence liquefaction, there is no credible pathway to scale. Building dedicated physical liquefaction infrastructure for every renewable molecule destined to maritime bunkering or long-distance use is neither economically viable nor environmentally sensible. It would multiply costs, duplicate infrastructure, and increase emissions associated with construction and operation for no system-level benefit. Equivalence liquefaction is the only mechanism that allows existing LNG terminals, gas grids and bunkering networks to be leveraged for renewable fuel delivery at the scale the maritime sector requires. Removing this option means removing the bridge between renewable methane production and maritime demand.

The investment case for biomethane and e-methane depends on it. Producers do not invest in new biomethane or e-methane plants based on a single end-use. They need a diversity of markets heating, transport, industry, and increasingly maritime to underpin the financial case. The maritime sector, driven by FuelEU Maritime and the extension of the EU ETS to shipping, has emerged as a major demand pillar. If this market is structurally penalized by an artificial GHG accounting framework, the investment signal for renewable methane production weakens across the board. The consequences extend far beyond bio-LNG and e-LNG: they affect the broader scale-up of renewable methane in Europe.

The window of opportunity is now. The European Commission is currently finalizing the revision of Annex VI of RED III and the consolidated Implementing Regulation 2022/996, both expected for public consultation in the coming months. These two acts, together with the parallel design of the UDB module for gaseous fuels and beyond 2026 for RFNBOs, will determine whether liquefaction by equivalence becomes a viable, scalable, certified pathway, or remains trapped in legal ambiguity that no economic operator can rely upon.

The choice is binary: either the EU framework explicitly recognizes liquefaction by equivalence on a non-discriminatory basis, with a coherent treatment across RED III, the Implementing Regulation and the UDB and bio-LNG and e-LNG can scale to meet maritime demand; or it does not, and an entire decarbonization pathway is closed before it has even opened.

For bio-LNG and e-LNG, this is not a regulatory detail. It is the difference between existence and irrelevance.

-----------------------

For more information, contact Mariana Tostes - mariana.tostes@eng-coalition.org

.jpg)

.jpg)

.jpg)